Factor Performance

This page presents performance results for the optimal factor specification identified by cross-sectional pricing tests using Liu et al. (2022) test portfolios:

Liu, Tsyvinski & Wu (2022) — VW, 2×3 double sort, sharp-year calendar

This configuration achieved the highest GRS p-value (best cross-sectional pricing) across 288 tested parameter combinations.

Sample: 2013-04-30 to 2026-02-19 (667 weeks)

Cumulative Returns

Summary Statistics

| Factor | Mean (%) | Median (%) | SD (%) | Skewness | Kurtosis | Sharpe (ann.) | t-stat | Min (%) | Max (%) | N |

|---|---|---|---|---|---|---|---|---|---|---|

| Market (CMKT) | 1.385 | 0.530 | 11.234 | 1.43 | 14.62 | 0.89 | 3.18 | -38.24 | 104.50 | 667 |

| Momentum (CMOM) | 0.219 | -0.397 | 16.027 | 1.05 | 40.55 | 0.10 | 0.35 | -159.92 | 168.06 | 662 |

| Size (CSMB) | 0.982 | -0.429 | 16.335 | 7.68 | 111.01 | 0.43 | 1.55 | -103.20 | 246.45 | 667 |

Factor Correlations

| Factor | Market (CMKT) | Size (CSMB) | Momentum (CMOM) |

|---|---|---|---|

| Market (CMKT) | 1.000 | -0.046 | 0.134 |

| Size (CSMB) | -0.046 | 1.000 | -0.023 |

| Momentum (CMOM) | 0.134 | -0.023 | 1.000 |

Return Distributions

Rolling Performance

Test Portfolio Performance

Size-Sorted Portfolios (Decile)

| Portfolio | Mean (%) | SD (%) | t-stat | Sharpe |

|---|---|---|---|---|

| D1 | 0.905 | 18.763 | 1.25 | 0.35 |

| D2 | 0.560 | 18.384 | 0.79 | 0.22 |

| D3 | 1.007 | 24.191 | 1.08 | 0.30 |

| D4 | 0.852 | 17.932 | 1.23 | 0.34 |

| D5 | 0.545 | 17.629 | 0.80 | 0.22 |

| D6 | 0.893 | 16.855 | 1.36 | 0.38 |

| D7 | 0.657 | 15.581 | 1.08 | 0.30 |

| D8 | 1.074 | 15.977 | 1.71 | 0.48 |

| D9 | 0.708 | 16.062 | 1.12 | 0.32 |

| D10 | 1.095 | 10.204 | 2.71 | 0.77 |

| 10-1 Spread | 0.332 | 15.297 | 0.55 | 0.16 |

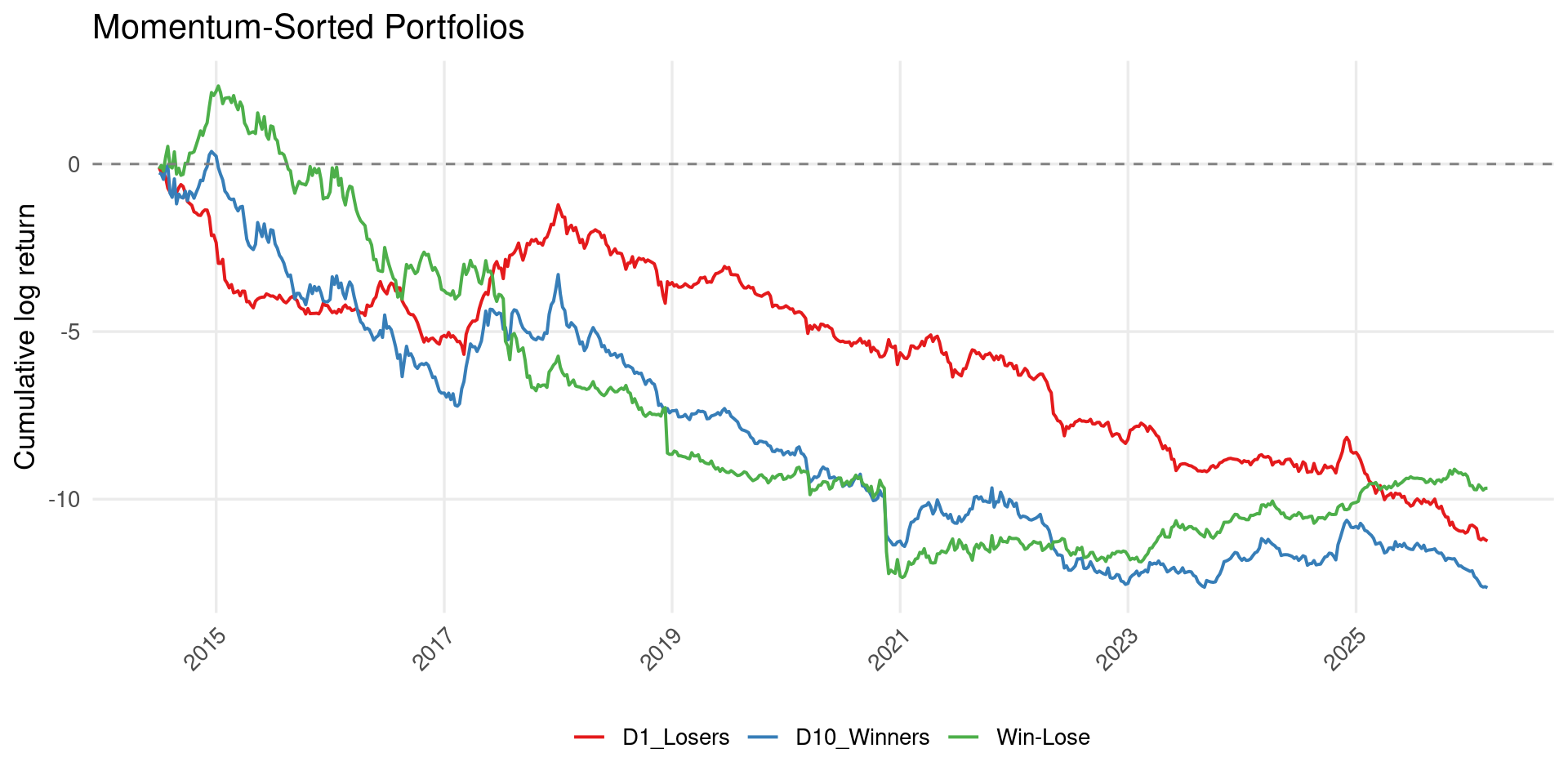

Momentum-Sorted Portfolios (Decile)

| Portfolio | Mean (%) | SD (%) | t-stat | Sharpe |

|---|---|---|---|---|

| D1 | -0.089 | 24.261 | -0.09 | -0.03 |

| D2 | -0.080 | 14.316 | -0.14 | -0.04 |

| D3 | 0.898 | 14.746 | 1.57 | 0.44 |

| D4 | 0.682 | 15.425 | 1.14 | 0.32 |

| D5 | 2.101 | 21.434 | 2.52 | 0.71 |

| D6 | 1.148 | 15.046 | 1.95 | 0.55 |

| D7 | 1.335 | 14.590 | 2.34 | 0.66 |

| D8 | 2.899 | 22.314 | 3.30 | 0.94 |

| D9 | 2.737 | 22.132 | 3.13 | 0.89 |

| D10 | 0.500 | 25.806 | 0.49 | 0.14 |

| 10-1 Spread | 0.581 | 27.622 | 0.53 | 0.15 |

Cumulative Portfolio Returns

Specification Details

This page displays results for the optimal factor specification selected via GRS cross-sectional pricing tests (details). The parameters are:

| Parameter | Value | Rationale |

|---|---|---|

| Weighting | Value-weighted | Best GRS p-value with Liu et al. test assets |

| Size breakpoints | Quintile (5) | Finer than median, less noisy than decile |

| Momentum lookback | 4 weeks | Strongest cross-sectional pricing power |

| Calendar | Monday-Monday | Slightly outperforms Liu et al. sharp-year |

| Exclusions | Stablecoins only | Wrapped/derivative exclusion has marginal impact |

| Delisting returns | Off | Synthetic -100% adds noise without improving pricing |

All other parameter configurations are available for download on the Download Data page.