Open Crypto Asset Pricing

Investable cryptocurrency risk factors — and an honest map of how much your specification choices matter

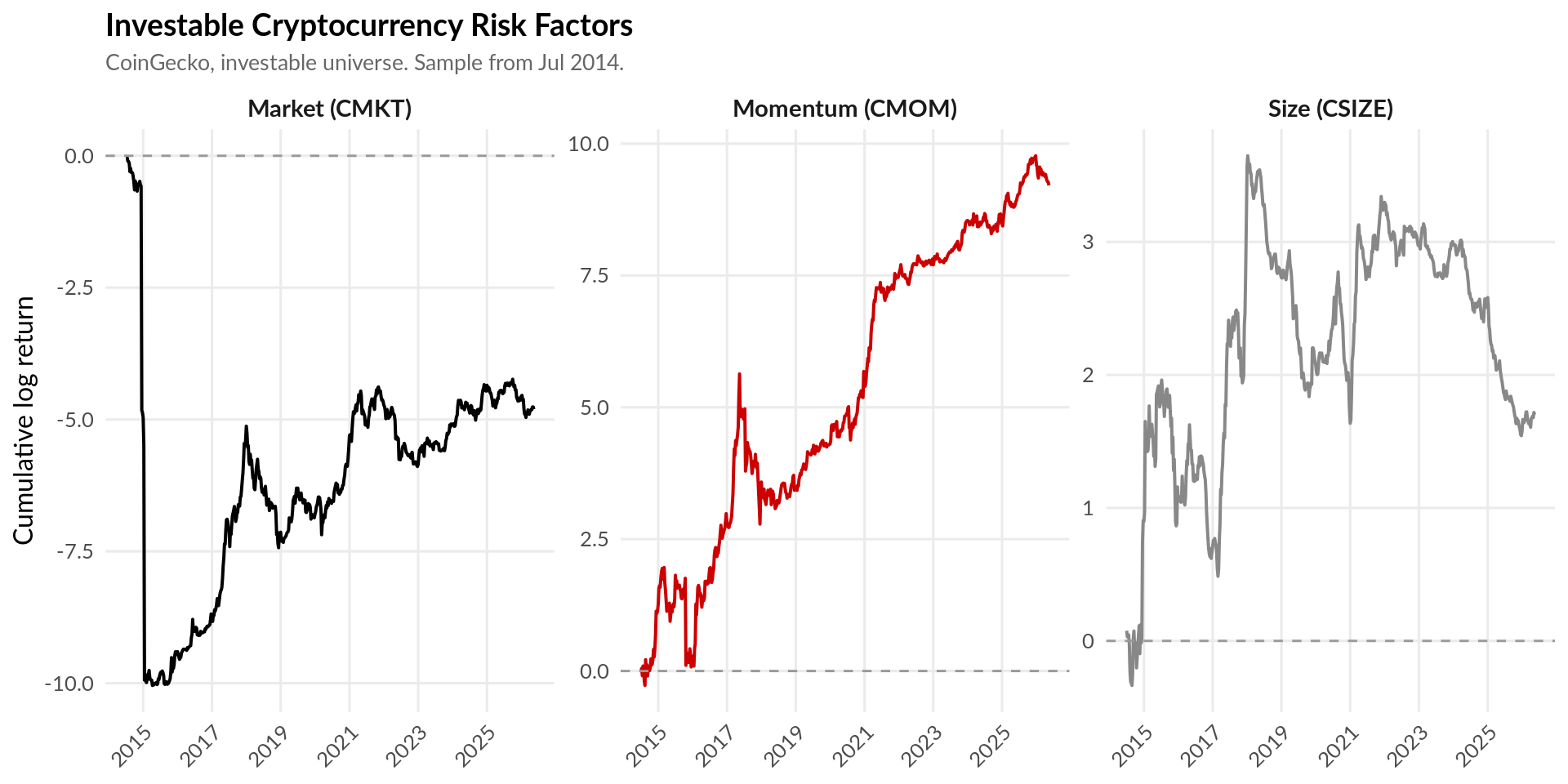

Open Crypto Asset Pricing provides free, openly constructed cryptocurrency risk factors — market (CMKT), size (CSIZE), and momentum (CMOM) — together with the evidence on how robust they actually are.

Our headline finding: the celebrated crypto size premium is an artifact of non-investable microcaps. Once breakpoints are computed on the investable universe, the size premium essentially vanishes; only short-horizon momentum survives and prices the cross-section. See the Results for the full multiverse evidence.

Coverage: 2013-04-30 to 2026-05-14 (679 weeks) · Updated: 2026-05-22

Use the factors in R

# CoinGecko & CoinMarketCap data via the crypto2 package

# install.packages("crypto2")

library(crypto2)

# Or pull the ready-made factor series directly:

url <- "https://opencryptoassetpricing.com/data/factors_cg_investable.csv"

factors <- read.csv(url) # week_start, CMKT, CSIZE, CMOMWhat you get

- Three factors (CMKT, CSIZE, CMOM), weekly, from two independent sources (CoinMarketCap & CoinGecko)

- Investable and full-universe (Liu-comparison) series

- The full specification multiverse: exclusions, calendar, weighting, breakpoints, momentum horizon

- Survivorship-bias free; transparent, reproducible construction

- Cross-sectional pricing tests (Fama-MacBeth, GRS) and factor-survival evidence

Quick links

Results

The investable cross-section: what survives.

Download

Factor & test-portfolio files.

Methodology

Construction & specification choices.

Data sources

Cryptocurrency data is retrieved with the crypto2 R package (CRAN) by Sebastian Stoeckl, which wraps both CoinMarketCap and CoinGecko. Both are survivorship-bias-free (delisted/inactive coins retained); we treat the choice of data source as one of the specification axes (see Results).

Citation

If you use these data, please cite Stoeckl (2026) and Liu et al. (2022).

References

Liu, Y., Tsyvinski, A., & Wu, X. (2022). Common risk factors in cryptocurrency. The Journal of Finance, 77(2), 1133–1177. https://doi.org/10.1111/jofi.13119

Stoeckl, S. (2026). Open crypto asset pricing. University of Liechtenstein. https://huggingface.co/datasets/sstoeckl/opencryptoassetpricing